Teaching Children the Value of Money: Pocket Money, Budgeting, and Early Financial Independence

Introduction

Teaching children the value of money through structured mechanisms such as pocket money, budgeting, and pathways to early financial independence forms a cornerstone of effective financial literacy education. Research consistently demonstrates that early exposure to these practices equips young individuals with essential skills for responsible decision-making, reducing the likelihood of financial vulnerability in adulthood. Parents and educators increasingly recognize pocket money as a practical tool for introducing concepts like earning, saving, and opportunity cost, while budgeting exercises foster long-term planning and self-discipline. This article draws on synthesized evidence from parental experiences, expert recommendations, and empirical studies to examine these methods, highlighting their benefits, implementation strategies, and outcomes in promoting financial independence.

Background: The Imperative for Early Financial Education

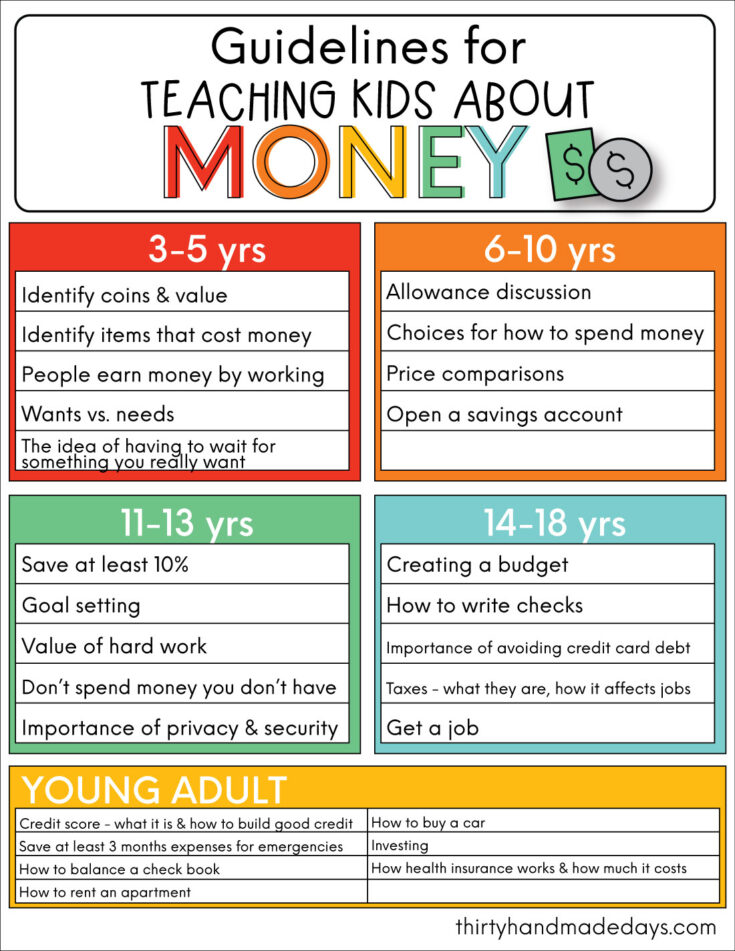

Financial literacy encompasses the knowledge and skills required to make informed decisions about earning, spending, saving, and investing. Children begin forming money habits as early as age 7, making this period critical for intervention. Without guidance, many young people enter adulthood unprepared, facing challenges such as debt accumulation or inadequate savings.

Empirical data underscore the long-term advantages of early education. Studies indicate that individuals exposed to financial literacy in youth exhibit improved asset accumulation, higher net worth by age 25, better credit scores, and lower debt delinquency rates. Programs emphasizing practical tools like pocket money correlate with enhanced budgeting, formal saving, and negotiation skills. These findings align with observations that financially literate young adults are more likely to maintain emergency funds, plan for retirement, and avoid financial fragility.

Contrasts emerge in global comparisons: while some regions achieve high literacy rates through integrated curricula, gaps persist where formal education is absent, leading to reliance on informal parental methods. This underscores the value of accessible, home-based approaches.

Current Findings: Pocket Money as a Foundational Tool

Pocket money serves as an entry-level mechanism for experiential learning, allowing children to manage a fixed sum while observing real consequences. Regular allowances, often starting around age 5–7 with small amounts, teach the finite nature of resources and the distinction between needs and wants.

Implementation varies: some families provide unconditional weekly sums to emphasize routine, while others tie payments to chores, reinforcing the link between effort and reward. Averages show weekly amounts increasing with age—for instance, modest sums for younger children (around £2–£5 in comparable data) rising to £7–£9 for pre-teens and higher for adolescents, accommodating growing responsibilities like social activities or personal items.

Benefits include improved decision-making, delayed gratification, and goal-setting. Children learn opportunity cost by choosing between immediate purchases and future savings, while exposure to scarcity builds discipline.

Digital tools enhance this process, offering prepaid cards and apps that track transactions, set limits, and gamify learning through missions on saving or budgeting. These platforms make abstract concepts tangible, particularly for older children transitioning to digital economies.

Here are illustrative examples of children engaging with piggy banks and allowance charts, demonstrating hands-on learning of money management:

These visuals capture the foundational joy and practicality of early financial habits.

Budgeting Practices and Family Integration

Budgeting extends pocket money by requiring allocation across categories such as saving, spending, and giving. Families often adopt simple splits—e.g., 50% save/50% spend for younger children, adjusting to 40% save/60% spend for teens with more expenses—to promote balance.

Real-life systems include comprehensive annual budgeting, where teenagers cover necessities (clothes, camps, entertainment) from a fixed monthly sum, teaching prioritization and forward planning. Such approaches mirror adult financial responsibilities, with children tracking expenses and adjusting for goals like events or purchases.

Parental involvement remains key: discussing family budgets openly demystifies finances, while games or apps reinforce concepts interactively. Challenges arise when children overspend, but these provide teachable moments on consequences and recovery.

Family budgeting sessions offer practical reinforcement:

Pathways to Early Financial Independence

Advanced practices bridge to independence, such as transitioning allowances to debit cards for real-world spending, or encouraging entrepreneurial ventures where earnings supplement pocket money. Teens managing full budgets for personal expenses develop accountability and foresight.

Digital platforms facilitate this by enabling goal tracking, interest visualization, and controlled spending, preparing adolescents for adult responsibilities like bill payments or investments.

Analysis and Implications

Evidence converges on pocket money's efficacy in building discipline and awareness, with budgeting enhancing planning and independence reducing long-term vulnerabilities. Minor contradictions appear in tying allowances to chores (some view it as motivational, others as conditional), yet overall consensus favors consistency and discussion.

Gaps include varying access to digital tools and cultural differences in implementation, suggesting tailored approaches.

Conclusion and Future Directions

Teaching children the value of money through pocket money, budgeting, and early financial independence yields enduring benefits, from enhanced decision-making to greater adult security. These practices, when applied thoughtfully, equip young people to navigate economic realities with confidence.

Future efforts should integrate formal curricula with home-based tools, addressing equity in access. By prioritizing these foundational skills, society can foster generations capable of sustainable financial well-being.

Comments (Write a comment)

Showing comments related to this blog.